2021 Tax Changes: What We Know Now (Updated)

Originally published January 6, 2021; Updated on April 12, 2021

2020: A Year of Tax Changes

2020 was a year filled with twists and turns - and that was certainly true for US tax laws too.

At the beginning of the year, the SECURE Act was put into place. This act was primarily established to make changes to the treatment and handling of retirement accounts. Some adjustments introduced were:

RMDs were pushed back to age 72 for those turning 70.5 in 2020 or later,

Contributions to IRAs, which previously had an age limit, are now allowed for anyone that is still working and receives earned income, and

Inherited IRAs now have a quicker withdraw requirement for non-spouse beneficiaries.

The year’s changes didn’t stop there. In response to COVID-19, the CARES Act was passed by Congress to provide economic relief across a wide range of avenues. From PPP loans to increased AGI limits on charitable contributions, the tax code changed significantly.

2021: A (Hopeful) Return to the Norm

With the hope that 2021 will come with fewer surprises, we will be reverting to some “normal” tax codes/requirements, including:

The reestablishment of required minimum distributions,

401(k) loan limits back to $50,000,

Imposed penalties on distributions from retirement accounts that fail to meet age requirements,

and more.

April 12 Update: It did not take long for tax changes to be instituted this year. On March 11th, President Biden signed the American Rescue Plan, and the IRS pushed the typical April 15th deadline to May 17, in response to that signing.

Tax Brackets & Standard Deduction

In 2021, tax brackets will look like those at the start of 2020. However, each bracket will increase by about 1% from the previous year, providing a marginal cost of living adjustment.

Standard deductions are growing from the prior year with married filing jointly and single filers allowed a $25,100 and $12,550 deduction, respectively. This is the primary choice for Americans.

If you do choose to itemize, be sure to save and keep records of your property taxes, medical expenses, mortgage payments, charitable donations, and more.

April 12 Update: The CARES Act allowed a $300 above-the-line deduction (2020 tax year) for those making cash contributions to qualified charities. For married filing jointly this has been increased to $600 (2021 tax year). This can slightly increase the deduction for those who choose not to itemize.

Popular Tax Credits

The Child Tax Credit is staying put at $2,000 for a child under the age of 17. This begins to be phased out at AGIs of $400,000 and $200,000 for married filing jointly and single filers, respectively. The credit for dependents who are not a qualifying child remains $500.

April 12 Update: The American Rescue Plan pushed the base credit to $3,000 and $3,600 for children under the age of 6. See blog for more details.

The America Opportunity Tax Credit can still provide up to $2,500 in tax credit per individual on $4,000 in qualified expenses (e.g. tuition). Modified AGI phase-outs are staying put at $160,000 and $80,000 for married filing jointly and unmarried individuals, respectively. Keep in mind, 40% of this credit is refundable.

The Lifetime Learning Credit can provide up to a $2,000 tax credit on qualified education expenses. For those not eligible for the America Opportunity Tax Credit this can be a beneficial alternative. The Modified AGI phase-out range for married filing jointly is up $1,000 from last year, now $119,000 - $139,000. The unmarried individual phase-out range did not grow from 2020 to 2021 ($59,000 - $69,000).

The Federal Adoption Tax Credit can now be worth up to $14,400 ($14,300 in 2020). This amount is not refundable so you may want to plan your itemization around an adoption event.

April 12 Update:

The Premium Assistance Tax Credit in 2021 can be eligible to those above the 400% Federal Poverty Level. For those who purchase health insurance through the state exchanges, you may be able to receive credits to offset some of those premium expenses.

The Child and Dependent Care Tax Credit in 2021 is getting a large upgrade. Maximum expenses for one or multiple children has been increased to $8,000 and $16,000, respectively. In addition, the maximum applicable percentage has increased from 35% to 50%, resulting in maximum potential credits of $4,000 for one child or $8,000 for two or more. These credits begin to fully phase out above $400,000 in AGI.

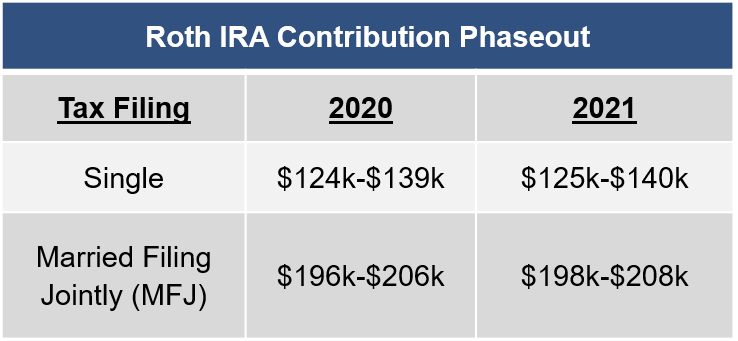

IRAs

Traditional and Roth IRA contributions limits will be the same as 2020 ($6,000) and the catch-up for individuals 50 or older is $1,000 ($7,000 total).

AGI phaseouts for Traditional and Roth IRAs:

You may get a tax deduction for contributions to a traditional IRA, or your AGI may qualify you for the increasingly popular Roth IRA.

Even if your AGI exceeds the phase-out limits you still have access to backdoor Roth IRAs by converting after-tax IRA contributions to a Roth IRA. Staying under the limits just makes the paperwork a lot simpler!

April 12 Update: Along with tax filing, IRA contributions for 2020 have been pushed back to May 17th (unless you have already filed taxes).

Retirement Plans

SEP IRAs are limited up to 25% of compensation or $58,000, whichever is less. Up from 2020’s dollar limit of $57,000.

Simple IRAs have not changed from 2020 to 2021. Employee contributions are limited to $13,500 and $3,000 for the catch-up (age 50+).

Like Simple IRAs, 401(k) and 403(b) plans will keep their 2020 limits as well ($19,500 and $6,500 catch-up).

Maximum defined benefit plan benefits are $230,000 for 2021.

Social Security

The maximum compensation subject to Social Security tax continues to grow at a strong pace; now up to $142,800 which is 3.7% greater than 2020’s $137,700 maximum amount. However, the cost-of-living adjustment (COLA) for 2021 benefits was only 1.3%.

Taxes on Medicare still have no limit.

The maximum monthly benefit at Full Retirement Age (FRA) is $3,148. Keep in mind, this can grow if deferred past FRA up to the age of 70.

Estate and Gifts

For the 10th year in a row, the estate and lifetime gift exemption will grow (now up to $11,700,000 per person). However, the annual gift exclusion remains at $15,000 for the 4th consecutive year. There are expectations that lifetime exemptions will be cut significantly in the coming years. You may want to consider some estate planning depending on your current and anticipated net worth.

Planning for 2021

Many people strictly do their tax planning at the end of the year, but we find it is best to get a head start. It is important to think about your income, giving, saving, and estate planning expectations for the upcoming year so that you can make decisions early to help optimize your tax bill and assets.

Perhaps 2021 is a good year to utilize annual gift exclusions early or to fund your monthly gifts for the year by donating long-term appreciated securities in January. Determine early whether you should be putting money into a Roth or pre-tax 401(k) and if IRA contributions make sense. If income is expected to be low, maybe 2021 will be a good year for Roth conversions.

Or maybe you need to get into the bi-annual routine of “clumping” tax-deductible items to get the maximum benefit. Or, use a Donor Advised Fund to capture increased benefits that come with charitable deductions.

If you need help putting the puzzle pieces together, please reach out to any of our team members at Kings Path. We would be happy to discuss how you can plan your taxes effectively, both in the short and longer term.